Business

Take control of employee spending with smart multicurrency cards

Let’s face it, managing your business expenses and employee spending can be very frustrating. Attempting to limit spend amounts or what your employees are spending company funds on; receiving complaints from employees who are “out of pocket” and haven’t been reimbursed yet because you haven’t had time; dealing with lost receipts; most of us agree, there must be a better solution that won’t break your bank.

Prepaid employee spending cards could be the answer to this. Compared with costly Expense Management platforms which often don’t fit SME budgets, they can be an extremely cost-effective option.

They’re also rapidly gaining in popularity.

What are prepaid cards?

Prepaid cards could be described as “stored-value debit cards” and can be used to pay for goods and services much in the same way traditional debit and credit cards can be. New generation cards are generally associated with one of the major card schemes such as Mastercard and Visa, meaning they’re widely accepted in the same places, provide the same “contactless” and “chip & PIN” technology and boast the same EMV security features.

How are they different to traditional debit and credit cards?

Prepaid cards store a value similar to a cash-wallet; only the value on the card can be spent until more funds are added. Spending limits can be controlled by simply limiting the amount added to each card making them arguably less risky than debit and credit cards.

Credit cards can attract interest and fees, especially if they aren’t paid on time which makes them more susceptible to unplanned charges than debit and prepaid cards. Debit cards usually don’t have the same fees incurred; however, it is possible to have your account overdrawn which could attract extra fees.

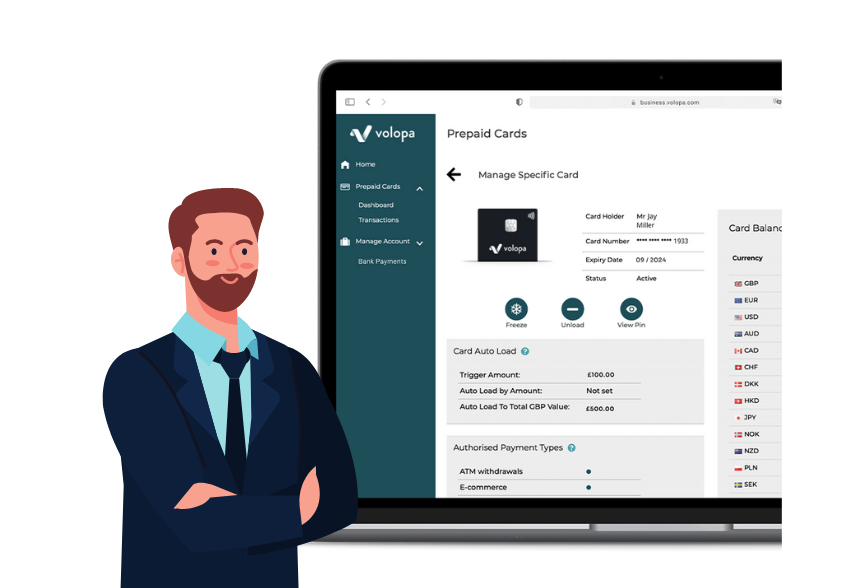

And "smart” prepaid cards?

Smart prepaid cards are commonly loaded and controlled via an app or online platform. This means you have real-time controls over load amounts, spending limits, spending transaction types, ATM withdrawal limits and have the ability to instantly freeze cards should they be lost or spending policies breached. A popular feature of a Smart prepaid card for employee spending is the ability to instantly add images of receipts as the expense is paid for and to add spending notes to allow easy spend-reviews and reimbursements. Like debit and credit cards, Smart prepaid cards can also be used to make purchases online.

Why would my SME use smart prepaid cards?

Current trends suggest that Smart prepaid cards may be the future of employee spend management. Providers such as Volopa offer the following benefits to make your life easier:

- Safer than carrying cash. If you lose your card, you can “freeze” it straight away via an app or website preventing anyone from using it and can move card funds back to your company wallet.

- You can control company spending. Easily control what your employees can spend company funds on, limit spend amounts and ATM withdrawal amounts and track spending in real-time.

- Load multiple currencies on Smart prepaid cards. With Volopa Business, you can add up to 14 currencies on a Smart Prepaid card at once making them ideal for travel. Your team can also sign up to Volopa Lifestyle for their personal travel and receive a free personal Smart card, app and cashback rewards.

- It’s easy to load and manage funds. It takes just seconds to transfer funds to your company wallet and then onto your individual cards. You can manage cards by user and easily transfer card funds back to your company wallet

- “Smart” spend-management Tools. Employees can take photos of receipts and add spend-notes which are instantly displayed in the company dashboard for the accounts team to reconcile.

- A low-risk way to trust your employees (not just the suits). Providers such as Volopa supply free Smart prepaid cards meaning you can empower your team with the ability to spend company money, knowing that you can track spending in real-time and you can freeze them instantly!

Conclusion:

Smart prepaid cards are a cost-effective way for you to take control of your employee spending and prevent your employees from being “out of pocket” having to spend personal funds. Volopa Business provides subscription free, no-long-contract Smart prepaid cards.

Find out more by emailing Business@Volopa.com or click on the button in the top right-hand corner to book your 15-minute live demo with one of Volopa’s London based team.

Securing the best exchange rates

Generally speaking, both banks and payments providers charge a margin, typically via a commission or a percentage-spread, for converting currencies from the funding currency (what you send them) to the payment currency (what the recipient receives). Banks are traditionally risk averse to currency movements due to the size of the portfolio of client assets they hold in multiple currencies. Any shock movement within the currency market can amount to significant losses, and in a bid to mitigate this risk, banks tend to apply higher margins.

International payments providers generally take a different approach, utilising live rates which they transact with immediately. Using this methodology, they don’t need to hold on to funds, the risk is less, and margins can therefore be much lower amounting to better exchange rates for their clients.

Payment Speed

Just as a bank cheque takes time to deposit into an account, so does sending money from one country to another. International FX payments can often take days to reach your recipient if sent via your bank. This is because banks often use manual currency conversion processes and tend to send funds via costly legacy banking networks. If you wish to transfer funds quickly, banks may not be your best option.

Specialist payments providers have established “points-of-difference” in the international payments market through innovative solutions to enable same-day international payments using more robust platforms and security systems. Specialist payment providers tend to route international payments via newer alternative payment rails that are quick, low-cost and easy to track, meaning recipients receive their payments in full and on time, while payment initiators can stay up to date with their payment statuses.

Conclusion

Whilst a bank may provide familiarity, specialised payments providers can offer better FX and payments expertise, superior technology and more cost-effective exchange rates. Through the tailoring of solutions and streamlining compliance requirements, services provided are largely more client-centric and focused. This often amounts to lower fees and charges as well as a superior customer experience for their clients.